Creatine is booming, but its subscription prize is already being claimed

Published June 2026

Published Jun 2026

Updated July 2026

Updated Jul 2026

6 min read

AI Summary

Pre-2023 supplement stores run 15x the subscription GMV of new creatine entrants, and the gap is widening. Based on data from 20,000+ subscription brands.

Create just raised $20 million to turn creatine into an everyday habit, and the whole category is sprinting after it. Creatine was the fastest-growing of the 200 most popular supplements in the US last year. Gummies and stick packs are everywhere. Create, for the record, runs its subscriptions on Recharge.

So if you sell supplements, the interesting question isn’t whether creatine is hot. It’s whether it’s too late to win it. Does when you entered the category actually change the economics, and by how much?

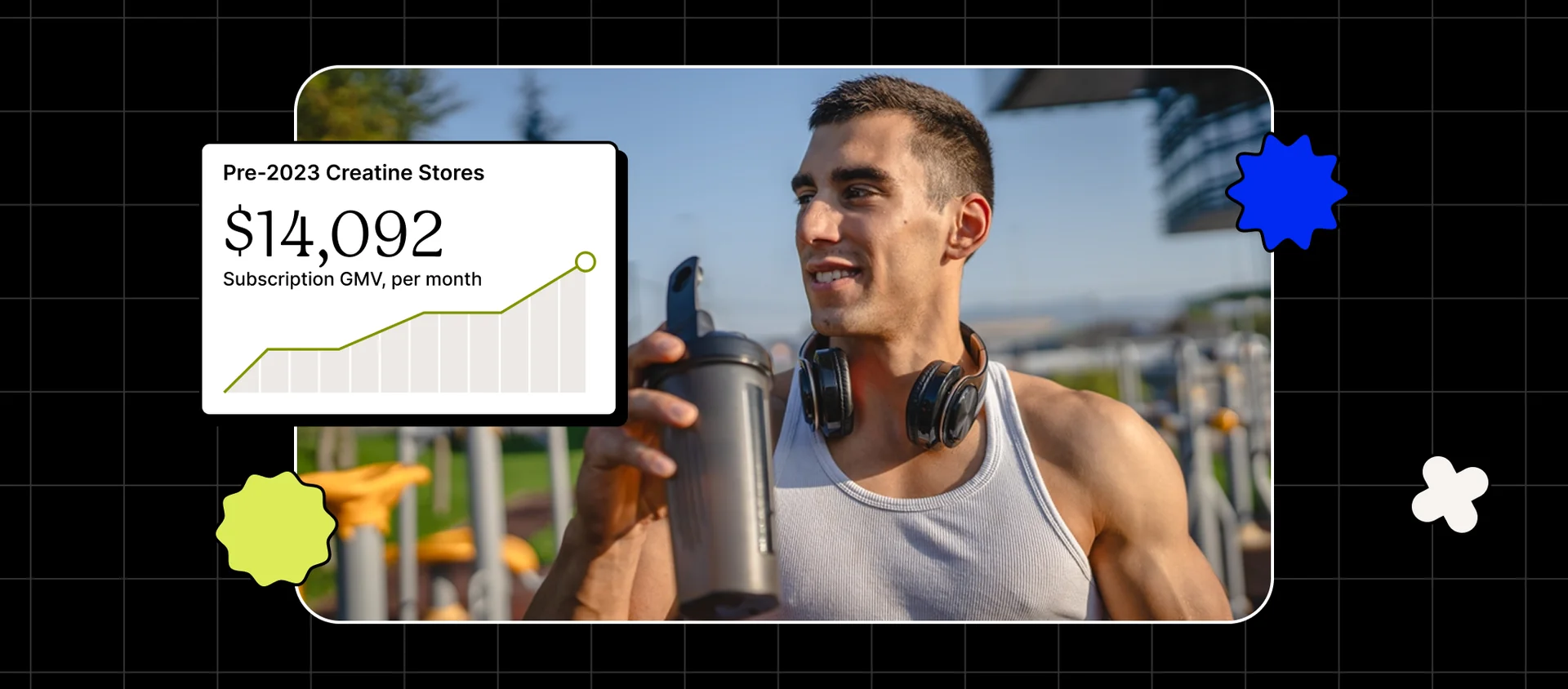

Our platform data has a blunt answer: in a commoditizing single-ingredient category, the subscription prize is largely already claimed. Among supplement stores that added creatine early, the ones live before 2023 run about 15x the median monthly subscription GMV (the gross sales a store moves through subscriptions each month) of stores that launched in the last 12 months. That gap is widening, not closing. Magnesium and greens, two categories that already ran this arc, show the same shape. Our take: the durable advantage goes to whoever turned the ingredient into a recurring habit first. To see where you stand, read your own subscription economics by store vintage, then compound the subscriber base you already have.

Does entry timing actually matter in a commoditizing ingredient?

It matters enormously. Pre-2023 supplement stores run about 15x the median monthly subscription GMV of last-12-month entrants, and the gap is widening.

By “vintage” we just mean when a store first went live and took its first charge. Sort creatine-selling stores that way and the spread is stark: stores live before 2023 run a median of about $14,092 in monthly subscription GMV, against roughly $955 for stores that launched in the last twelve months.

That pattern isn’t unique to creatine. Magnesium and greens, two single-ingredient categories that already crossed from niche to mainstream, show the same early-mover spread. And in every one of them the gap is wider than it was in our prior study, not narrower. Newcomers are entering smaller and staying smaller.

| Category | Pre-2023 (early) | Last 12 mo (late) | Gap | Prior (May ’26) |

|---|---|---|---|---|

| Creatine | $14,092 | $955 | 14.8x | 8.5x |

| Magnesium | $10,162 | $1,148 | 8.9x | n/a (new) |

| Greens | $9,214 | $2,271 | 4.1x | 3.4x |

Across all three, the early-versus-late gap is wider than the prior study. The lead isn’t eroding as these categories mature. It’s growing.

Is that a stickier subscriber, or just a bigger book?

Mostly a bigger book. The early-mover edge is scale and a mature subscriber base, not a dramatically stickier subscription.

It’s tempting to read a 15x revenue gap as proof that early subscribers are far more loyal. The retention data doesn’t support that story. Strip out the newest cohort’s immature book (44.5% of their renewal cycles are still “outstanding,” too recent to have resolved) and compare like for like: pre-2023 stores process about 71.3% of resolved renewal cycles, against 64.7% for the newest cohort. That’s a real edge, but a modest one, about six points.

| Vintage | Process rate (resolved) | “Outstanding” share |

|---|---|---|

| Pre-2023 | 71.3% | 2.2% |

| Middle (2023 to mid-2025) | 68.9% | 1.9% |

| Last 12 mo | 64.7% | 44.5% |

So the chasm in GMV isn’t coming from dramatically lower churn. It’s coming from scale and maturity: more subscribers, accumulated over more time, on a habit that’s had longer to compound. One caution on the table above, don’t read the newest cohort’s low resolved volume as churn; those subscriptions are simply too new to have run their course.

Are late entrants catching up?

They aren’t. Each successive entry wave steps down, with no sign of convergence.

The cohort that launched between 2023 and mid-2025 sits at about $8,971 in median monthly subscription GMV. That’s already 9.4x the last-twelve-month cohort, and only about 1.6x below the pre-2023 leaders. Read the three waves in order and they descend in a straight line. The gap doesn’t close as the category matures. It widens as the category floods.

The most plausible explanation is habit. Whoever got subscribers onto a recurring creatine order first built an install base that keeps compounding, and later entrants are fighting for what’s left. Worth one honest caveat: this is an association, not proof of cause. Older, larger, surviving stores sit in that early cohort, and some of the advantage is simply maturity and survivorship.

What should subscription operators take from this?

If you already sell in one of these categories, the lead is real and it compounds, so the move is to read your subscription economics by vintage and compound the base you already have.

Pull your own numbers the way we pulled these: by store vintage and product cohort, over time, not just this month’s topline. Recharge’s subscription analytics are built for that read. Then act on the base you’ve got. The growth in these categories lives inside existing subscriptions, so cross-sell and build-a-box offers to current subscribers are where the lift is, and protecting that base with the right churn-prevention tools keeps the compounding intact. Our broader Subscription Trend Report tracks these category shifts if you want the cross-brand view.

If you’re weighing whether to enter, the data isn’t telling you to stay out. It’s telling you the prize is the habit-formation window, not the launch. Design for ritual fit, and get subscribers onto a recurring cadence fast, because that’s the edge that’s still open.

tl;dr… in a commoditizing ingredient, the durable advantage goes to whoever built the recurring habit first. Read your subscription economics by vintage, and compound the subscribers you already have.

About this report

These insights come from creatine-, magnesium-, and greens-selling stores on Recharge, all actively running subscriptions on Shopify, with hundreds of stores in each category.

The window is the trailing twelve months, June 2025 through May 2026, with each store grouped by when it first went live.

Every figure is a median across stores and aggregated, so no single merchant’s numbers appear. GMV is measured at the whole-store level, which is why we read it as “supplement stores that added creatine early,” not pure-play creatine brands. And one caveat to flag: the early-mover gap is consistent with habit lock-in, but it isn’t proof of cause. Merchant maturity and survivorship are part of the picture.

FAQ

Is it too late to launch a creatine subscription brand?

Not necessarily, but the durable advantage concentrates in early movers, so a late entrant has to win on habit formation and ritual fit. The category’s growth won’t lift everyone equally.

Does entering a supplement category earlier actually improve retention?

Slightly. Resolved renewal process rates run about six points higher for pre-2023 stores. The larger early-mover advantage is scale and subscriber-base maturity, not dramatically lower churn.

Categories

Related articles

Explore additional content that complements what you’ve just read.

The first-order discount sweet spot for CPG subscription brands is deeper than you think

There’s a fresh wave of pet-food M&A, and the subscription data shows what’s actually worth the premium

Menopause: the unsexy subscription category that outlasts fertility

Electrolyte brands are multiplying faster than their subscribers

How do backup payment methods affect involuntary churn?