Electrolyte brands are multiplying faster than their subscribers

Published July 2026

Published Jul 2026

3 min read

AI Summary

Electrolytes are one of the hottest bets in consumables. The category’s drinks market is tracking toward roughly $43 billion in 2026, according to Fortune Business Insights, and it feels like a new hydration brand launches every week.

Electrolytes are one of the hottest bets in consumables. The category’s drinks market is tracking toward roughly $43 billion in 2026, according to Fortune Business Insights, and it feels like a new hydration brand launches every week.

So here’s the question a founder eyeing the category should be asking: if everyone is piling in, is there room left, and will the subscribers stick once you have them?

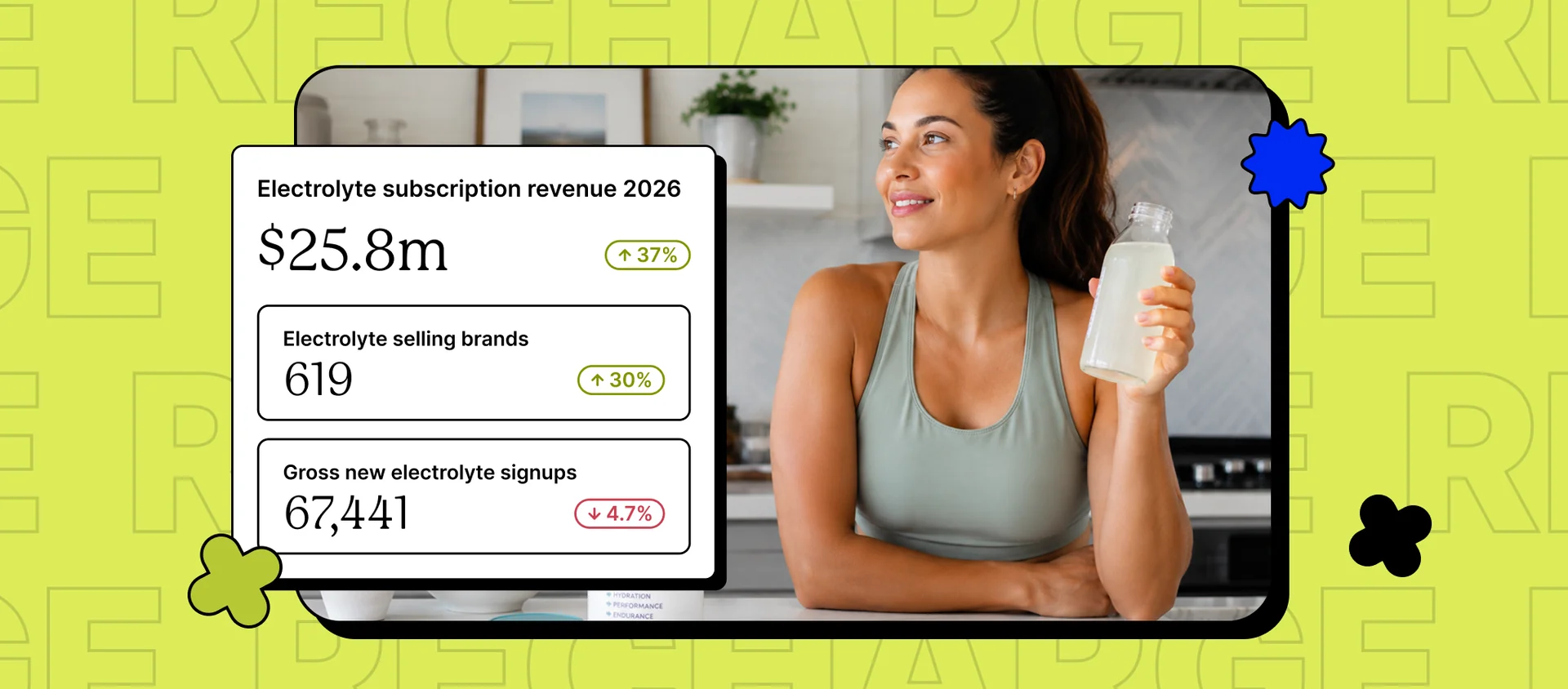

A year of electrolyte subscription data on our platform tells a sharper story than the market charts. Comparing this spring to last (a clean read, since hydration always spikes with the January new year, new me crowd), brands running electrolyte subscriptions grew 30% and category subscription revenue grew 37%. But new subscriber signups stayed roughly flat, and the average order size didn’t move. So more brands and more revenue are chasing the same trickle of new subscribers, and each brand’s slice is thinner than the category headline suggests.

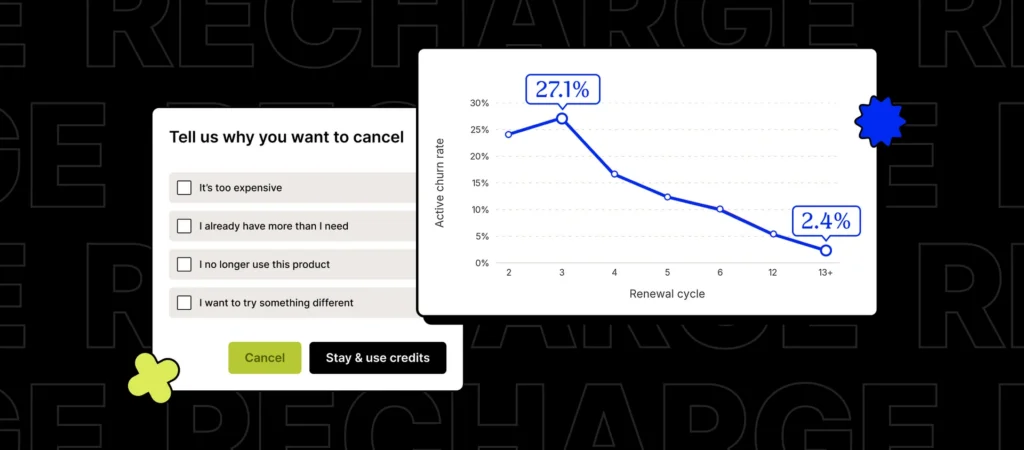

And the ones who do sign up don’t stick around long. Churn runs high, and 90% of it is voluntary, people choosing to cancel rather than a payment failing. Don’t get it twisted: the demand is there, it’s just not expanding fast enough to go around. The real edge in electrolytes is holding onto subscribers through those first few orders.

| Electrolyte subscription category (YoY, spring 2025 to spring 2026) | Change |

|---|---|

| Brands selling electrolyte subscriptions | +30% |

| Category subscription revenue | +37% |

| New subscriber signups | Roughly flat |

| Average subscription order value | Flat |

So what do you do about a leaky category?

Treat the first order as the opening move and build from there. The highest-leverage moment is the cancel screen, since that’s where voluntary churn happens, so meet subscribers there with a reason to stay through cancellation prevention. Keep the box from getting stale, since flavor fatigue tends to hit around order three, by letting people rotate flavors and formats with build-a-box options. And track your own order-to-order retention in subscription analytics, because the category benchmark only helps once you know where you stand against it.

What to do with this

Assume acquisition will be a knife fight and make retention your edge. Fight cancels at the cancel screen, keep flavors fresh, and judge the program by how many subscribers reach order five. Our subscription trend report has the cross-category view, and food and beverage brands can see where electrolytes fit on our food and beverage page.

tl;dr: Electrolyte brands are multiplying 30% year over year and category revenue is up 37%, but new signups are flat and most churn is voluntary, so keeping subscribers matters more than adding them.

About this report

This looks at brands selling electrolyte and hydration products on the Recharge platform, comparing two matched spring windows a year apart. All figures are category-level aggregates across hundreds of brands. Signups held roughly flat year over year rather than rising, so read this as a category getting more crowded rather than one adding new subscribers.

Categories

Related articles

Explore additional content that complements what you’ve just read.

The first-order discount sweet spot for CPG subscription brands is deeper than you think

There’s a fresh wave of pet-food M&A, and the subscription data shows what’s actually worth the premium

Menopause: the unsexy subscription category that outlasts fertility

How do backup payment methods affect involuntary churn?

Subscription churn is front-loaded: the first reorder matters more than acquisition